Table of Contents

Paul Frijters

Gigi Foster

Michael Baker

brownstone.org

Paul Frijters is a Professor of Wellbeing Economics at the London School of Economics: from 2016 through November 2019 at the Center for Economic Performance, thereafter at the Department of Social Policy

Gigi Foster, senior scholar of Brownstone Institute, is a Professor with the School of Economics at the University of New South Wales, having joined UNSW in 2009 after six years at the University of South Australia.

Michael Baker has a BA (Economics) from the University of Western Australia. He is an independent economic consultant and freelance journalist with a background in policy research.

Warning

Long read: 2665 words

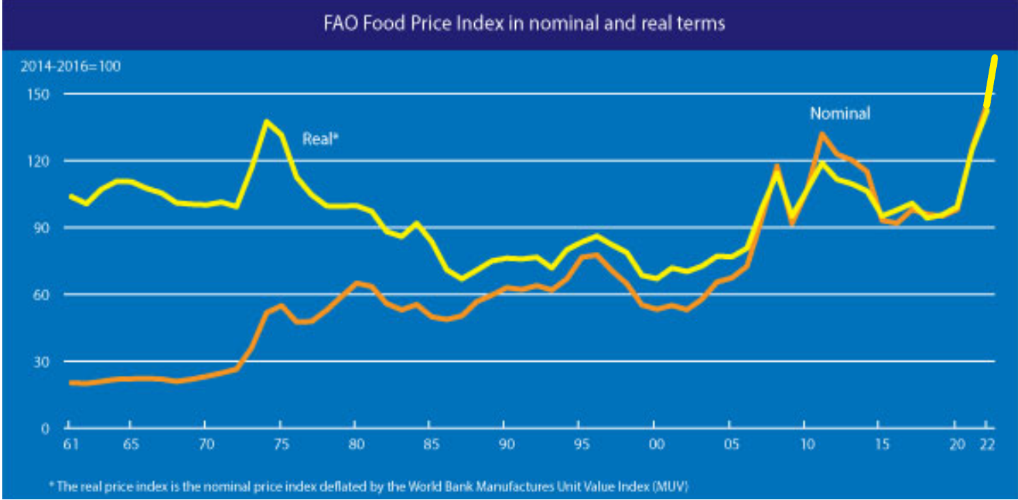

The latest index of world food prices was released by the UN’s Food and Agriculture Organisation (FAO) on 8 April. The FAO’s Food Price Index climbed to 159.3 in March, which in real terms is roughly double its level in 2000, about 80 per cent above its 2019 level, and the highest since records began in 1961.

This graph indicates that civil war and famine in poor countries are now inevitable. World food prices were already 40 per cent above pre-lockdown levels at the start of 2022 due to supply chain disruptions, caused largely by Covid containment measures instigated by governments around the world.

Factories closed and work forces were told to stay home even when they weren’t sick. Shipping costs increased because of arbitrary port closures that diverted containers and ships to the wrong places, so exporters struggled to find containers and when they did they couldn’t find ships to put them in. Food rotted in warehouses.

Then came the war in Ukraine, pushing the food situation into even more acute crisis mode.

While the world has plenty of spare food-growing capacity, it takes a few years for additional production to materialise. Existing farms can only slowly increase productivity or bring more land into cultivation. It only takes a month without food for a person to starve to death though, so a two-year food crisis means human catastrophe.

Some propagandists will point the finger at China, which is believed to have huge stockpiles of rice, maize and wheat – perhaps more than half the world’s reserves. Yet it has had those reserves for almost 10 years now. The Chinese have not suddenly bought up food since March 2020 in order to cause wars elsewhere.

How much political unrest is coming our way as a result of the global food shortage? A 2015 paper on the riots caused by food price spikes in 2007-2008 and 2010-2011 found that about two serious riots per month occurred when food prices rose 50 per cent above previous levels. Four to six riots occurred when prices doubled.

Food price levels in early 2022 were already a full 30 per cent above the post-GFC peak, while real GDP per capita for poor countries (see here, for example) was about the same as in 2008 but with much greater inequality. This combination is the core reason why Oxfam in its paper of April 12, entitled “First crisis, then catastrophe”, calculated that close to a billion people in 2022 will be in extreme poverty, facing hunger.

With food prices now a third higher than those that helped spawn the 2011 Arab Spring, we are already seeing food used as a political weapon in Ethiopia, Yemen and elsewhere. We will undoubtedly see this much more in 2022. Places like Afghanistan and the poorer parts of Africa may well explode politically, as the Famine Early Warning Systems Network is documenting.

Can WEIRD (Western, Educated, Industrialised, Rich, Democratic) countries stop this train?

Rich Western governments have historically been associated with high levels of social stability and low levels of violence. Are they willing and able to use their riches to contain the consequences of the post-Covid famines? Or are they going to be too preoccupied with their own financial problems, wrought by their ailing tax systems and two years of throwing money at misguided Covid containment efforts?

The answer is disconcerting, to say the least.

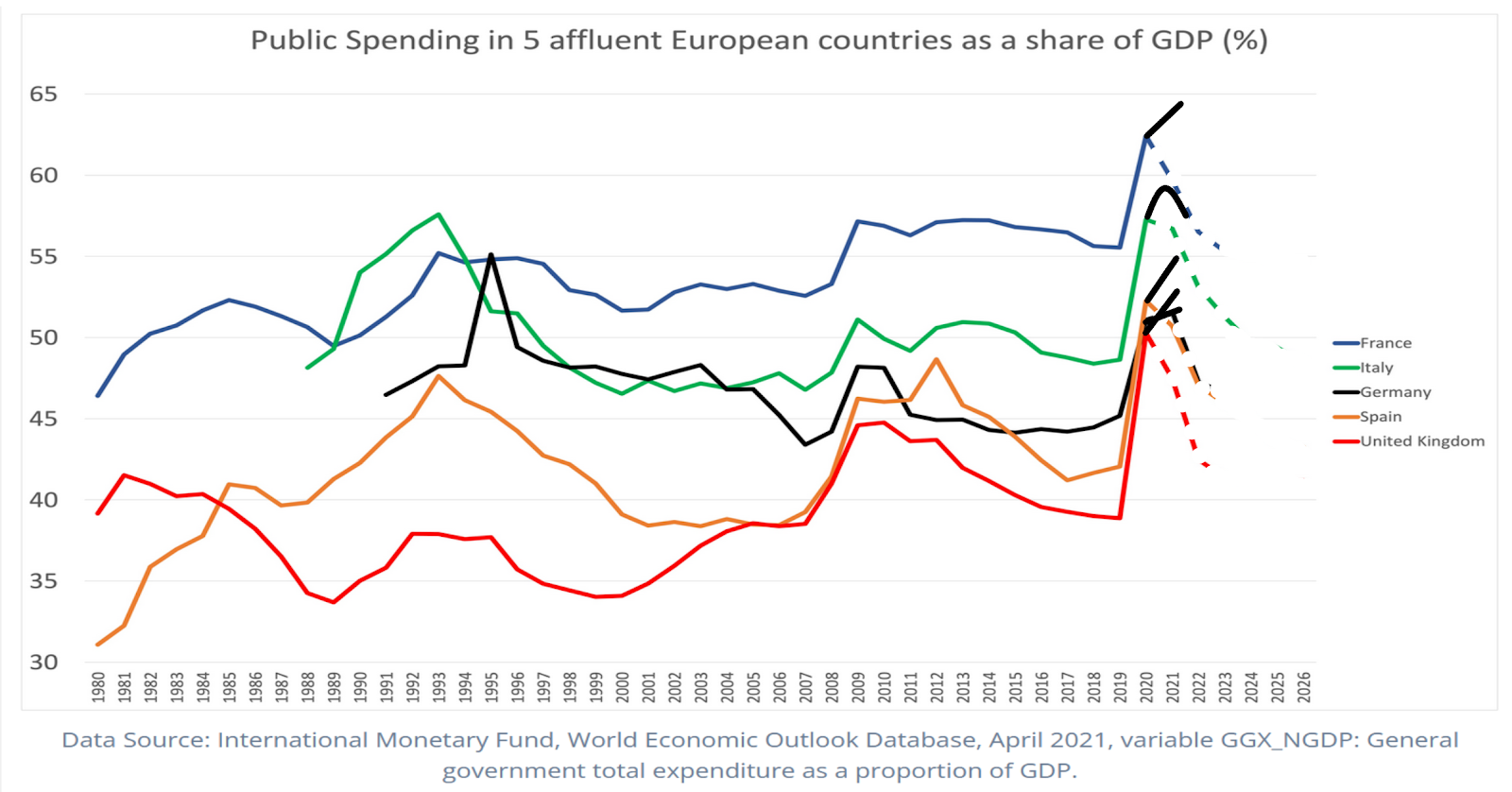

The graph below tracks government spending in five major European countries up to and including 2020. The dashed lines after 2020 show what governments said they expected to happen, while the solid lines approximate what has actually happened, through the end of 2021.

During this period, government revenue has hardly moved, so the extra spending came from more government debt. Debt-to-GDP ratios are rising by about 10 GDP percentage points annually in the EU and the US, more quickly in some places (France, Anglo countries) than others (Scandinavia).

Instead of the predicted decline in government spending after the 2020 rise, the continued escalation of spending in 2021 was spectacular in some countries, such as the UK, France and Spain. These increases were partly driven by spending on defense and social programs (pork barrelling in advance of important elections in France and Spain), but more particularly by the ongoing Covid circus that has led to unproductive spending on all the usual paraphernalia (vaccines, masks, tests…) and on the bloated control apparatus that is hanging on to its budget for dear life.

Government spending is higher now than ever before for most of these countries. It is at levels long deemed unsustainable. If you doubt this, consider that the Reagan/Thatcher privatisation reforms of the 1980s and 1990s were preceded by government spending peaks of ‘only’ 50 per cent of GDP.

The tax base problem

Governments have been spending more than they are able to tax. Economists would say that we are now on the right-hand side of the Laffer curve, meaning that attempts to tax more will induce so much tax avoidance that tax revenue will fall. The logic is easy to see in the extreme case: if you tax an activity at 100 per cent, then that activity stops and you get $0 in tax take.

When he was once asked why he robbed banks, Willie Sutton said “Because that’s where the money is.” The problem for government tax collectors today is that, unlike Sutton, they can’t get near enough to where the money is.

The problems in taxation are deep and long-standing, partly because the super-rich in charge of the biggest corporations, who own more and more of the world’s wealth, have escaped the tax net and are able to pressure governments they don’t like by funding media campaigns against politicians who try to tax them. Not being able to get a fair share of taxes from the wealthy is a major political problem, made worse by the enormous demands on the public purse just to keep the Covid carnival going.

There’s only one way out for all the governments caught between their inability to tax those with the money and the expensive demands of health theatre, and that is to print money. Governments have engineered this by selling debt (bonds of varying maturities) to their own central banks.

What happens when you do this without the production increase to back it up? As we predicted at the end of 2020, the result is inflation, which reduces the real value of money. Inflation caused by money-printing can be viewed as the government taking a cut from everyone who uses that currency. This effect, called seigniorage tax, amounts to taxation by desperate authorities that have lost control over the super-rich who no longer pay their taxes.

How long can desperate governments keep on taxing populations via printing money? Only as long as populations cannot find another currency in which to transact. If a switch is possible, people stop using the currency that is being taxed so heavily, hyper-inflation arrives and a horrific economic meltdown ensues as governments go bankrupt and populations are impoverished.

This problem is particularly pernicious for the EU, and somewhat less so for the US, which is in the fortunate position of having the world’s global currency (about 60 per cent of international financial reserves are in US dollars) and thus being able to wring a good amount of seigniorage taxation out of the rest of the world, although this is slowly reducing over time.

The big political game in the West, and particularly in the EU, right now is how to prevent populations from running away financially. If they do, it will usher in a collapse of the EU and its finances. That would place us smack in the middle of the 1930s again, with all sorts of fanaticism ruling the roost and no endpoint until government spending is vastly reduced and the super-rich are brought to heel.

This journey can be expected to involve millions of deaths as the fanaticism created runs its course. This scenario has become more likely over the last 12 months as many governments have found they cannot wind back spending.

Private rating agencies like Fitch are waking up to this and have almost doubled their estimates of inflation in the EU in April 2022 relative to December 2021, while also predicting that European countries are going to try to spend their way out of the current crisis.

The European Central Bank (ECB) is simultaneously expected to stop buying up government bonds, thus allowing only countries that are trusted by markets to pay back their debts to borrow more. That means places like Italy will not be able to borrow more and will have to make dramatic spending cuts, while places like Germany can keep borrowing for a while yet. Riots in Rome, but not in Berlin.

The role of digital passports and currencies

The provision of stability by democratic Western states has traditionally been possible because of state spending on core services and institutions that enable markets to thrive. With all the extra debt-financed spending of the past two years on largely unproductive things, and now their tax base receding, where will nations get the fuel to burn in the fight to maintain political stability in the coming years?

To prevent a complete collapse of their tax base, governments (particularly in the EU) are desperately trying to force populations into using only approved currencies so that they can keep on taxing them.

This is the economic rationale behind digital passports, digital currencies and populations having central government bank accounts: the hope of the authorities is that full digital observation of their finances will prevent people from switching to a form of money that cannot be taxed by having more of it printed.

The levers for such control include paying civil servants only in approved currencies, paying all welfare and other government expenses in those currencies, forcing all companies in their purview to pay their bills and staff in those currencies, and forcing as many consumer transactions as possible to be in those currencies.

A digital monetary dictatorship is the goal. If the super-rich cannot be taxed through governments observing what they own, then perhaps every trade with the super-rich can be taxed by forcing those trades to happen in an approved currency. There’s logic to it.

Enormous control is needed for this to work because populations, and particularly their richer and more dynamic elements, will seek ways to avoid the taxation. Things that are not taxed will start to be used as money – land, houses, gold, wheat, oil, grandma’s silver, etc. Anything that is itself worth something can start to be used as money, either through paying with it directly or as collateral. Such on-the-sly trades will be easier for smaller companies and harder for larger ones that cannot escape the gaze of government.

Gradually, an alternative underground banking system would emerge in which people trade in untaxed currencies that are either trusted (the Chinese Yuan? A currency put out by companies – eg a “Big Tech Dollar”?) or backed up by commodities.

Locally and in bilateral trade between countries (such as Russian or Iranian oil in exchange for the Yuan), people would opt for untaxed currencies and would also start bartering with each other, doing favors in exchange for food or other goods. The wedge would widen between what the state can observe and force into its currency system, versus its alleged sphere of influence.

We are already seeing this dynamic erupting on the international stage, with Russia moving away from dollar-pegging and towards commodity-backing, in a retreat back to the norm of the pre-1971 Bretton Woods system. Though we don’t think this move is sustainable, the development is ominous.

If enough other countries follow China and Russia in their retreat from the US dollar, then the US government will eventually be unable to tax the rest of the world, by printing more dollars and thereby seigniorage-taxing all holders of dollars (including many foreign countries), and will be confined to taxing only domestic transactions that can be forced to use dollars. The same would hold for the EU and its Euros.

People are already looking for land, commodities and property to buy so as to avoid the consequences of government money printing. The super-rich are leading this charge, as they can afford the smartest advisors who will have told them all the above more than a year ago.

The limits of governments’ financial controls

Will the US and the EU monetary authorities manage to force their populations into using their preferred digital currencies? They will struggle. Capital flight into commodities and ‘safe’ countries, like Scandinavia and Switzerland, can be fought, but only with capital controls in addition to new taxes on commodities as those commodities replace money: taxes on houses, taxes on land, taxes on gold.

That race would cause chaos because many such commodities are highly leveraged. The middle classes in most countries would be financially ruined if they would have to pay high interest rates on their mortgages or significant recurring taxes on their houses.

Every country that has made the political choice to print money in order to hide the fact that its Covid policies have reduced the productive part of the economy, while increasing the government sector by spending on useless control measures and health theatre, now stands at a financial cliff. We fear that major recessions, at the very least, are in store for such countries while their governments get their act together. The possibility of helping those starving and rioting overseas will simply be erased by domestic disaster.

What scapegoats will governments offer for all this? The old chestnuts they already blame: climate change, the Russians, the pandemic, China, internal critics, the unvaccinated, populism and so on. Anything but themselves.

So far, populations have largely swallowed this story, assisted by Big Tech, Big Pharma and others that have worked diligently to ensure that people believe the problems are unrelated to current ideology and politics.

That propaganda comes with its own price, because populations that believe it then demand even more forms of self-harm – eg more restrictions on travel and trade ‘to save the planet’. All kinds of self-harm are now being bandied about as ‘solutions’, pushed by political elites scrambling to avoid responsibility for their disastrous choices.

The propaganda is powerful, but reality is still slowly intruding into this make-believe world. Increased food and fuel prices, general inflation, reducing services and economic hardship cannot be painted over, and the limits of money printing have been reached. Such are the fruits in developed nations of the Great Covid Panic, just as famines are its fruits in poor countries.

Civil wars and famines in 2022 are a near certainty for many poor countries, while the West is preoccupied by trying desperately to avoid its date with financial destiny and is out of money, even if it wanted to help.

This year looks like being a year of reckoning for the Covid madness of 2020-2021. We fear the reckoning will involve even larger-scale madness than we have seen so far. The Furies have taken flight.

{kind=link}