Table of Contents

The Dashboard will provide a regular snapshot of economic conditions as they are developing.

High-frequency indicators show that economic activity continues to run at much lower levels than normal under Alert Level 4. New Zealand will move to Alert Level 3 from 28 April, where it will remain for at least two weeks. Businesses will be able to resume operations if they are contactless, and a substantial part of the workforce will be able to resume work, but economic activity is expected to run around 25% below normal levels at Alert Level 3. Numbers of Jobseeker Support recipients have risen sharply, and while inflation reached a 9-year high in March, it is set to decline substantially this year. Global dairy prices have fallen.

Global growth in active cases of COVID-19 continues to slow, which has prompted some European countries to come out of lockdown. High-frequency indicators suggest US economic output is 11% lower than last year. China’s GDP was 6.8% lower in the March quarter than the same quarter a year ago. US oil prices went into negative territory this week for the first time in history due to excess supplies and insufficient physical storage capacity. Governments around the world continue to provide further monetary and fiscal stimulus.

With the chain of transmission now broken…

On 20 April, the Prime Minister announced that New Zealand has successfully broken the chain of transmission of COVID-19. New cases on 23 April numbered just three, and active cases have declined for two weeks (Figure 1). Seventy percent of COVID-19 cases in New Zealand have now recovered.

Figure 1: Daily COVID-19 cases in New Zealand

…businesses can prepare for Alert Level 3…

With lockdown restrictions set to ease, the Government has allowed businesses to re-enter their premises to prepare to re-open safely if they can under Alert Level 3. Only businesses that can introduce physical distancing and contactless transactions will be able to open next week.

Around half a million people are expected to be able to return to their workplaces in the coming weeks. Treasury estimates that economic activity will run approximately 25% below normal levels during Alert Level 3, higher than under Alert Level 4 (Figure 2). Some retail and hospitality activity will resume, but many businesses will remain closed. A recent survey conducted by the NZ Restaurant Association found that only one third of hospitality businesses plan to reopen.

Figure 2: Estimated economic activity at Alert Levels

…but the lockdown is not over yet

Light and heavy traffic in New Zealand’s main centres remain well below 2019 levels (Page 2). Although volumes appeared to tick up over the weekend, this is relative to Easter weekend in 2019, which came a week later. On 22 April, no international passengers arrived in New Zealand for the first time in decades.

On 17 April the number of Jobseeker Support beneficiaries reached 175,000, around 5.8% of the working-age population, up 1 percentage point since 20 March. Total wage subsidy payments totalled $10.1 billion, benefitting 1.6 million people.

High-Frequency Indicators (under development)

Statistics NZ has recently released a portal where people can download a range of high-frequency indicator series. This portal can be accessed at:https://www.stats.govt.nz/experimental/covid-19-data-portal

Traffic Movement

Border Crossings

Job Seeker Support

Freight Movement

Retail Spending

Fiscal Support: Wage Subsidy (paid)

Inflation reached its highest rate since 2011…

Annual inflation in the March quarter was above expectations at 2.5%, up from 1.9% in the December quarter, reaching its highest annual rate since 2011 (Figure 3). Quarterly inflation was 0.8%, driven by a 1.4% rise in non-tradables prices. Non-tradables inflation reached a 9-year annual high of 3.4%. The increase was driven by higher housing rents and cigarette and tobacco prices, which contributed 0.4 and 0.3 percentage points respectively to headline inflation. Tradables prices rose 0.1% in the quarter, to be up 1.5% annually. Higher prices for grocery goods and fruit and vegetables were partly offset by lower transport costs, particularly petrol. With weak oil prices expected to persist, tradables inflation is expected to ease next quarter.

Figure 3: Annual Inflation

The latest inflation reading is above the Reserve Bank’s target mid-point of 2.0%. However, the measures that have been put in place to contain the spread of COVID-19, including closing our border to international travellers, freezing housing rents for six months from March, and only allowing essential business activity for most of April, will lower economic activity and reduce demand. Wage cuts and job losses as a result of COVID-19 are also expected to contribute to a reduction in spending and an increase in precautionary saving for some time.

Prices have also been impacted by international developments. World oil prices have reached historical lows, with WTI in negative territory for the first time in its history (Figure 4). While lower oil prices would usually translate to lower domestic fuel prices, there will be a limit to how low they can go given the sort-run nature of the reasons for the sharp price drop.

Figure 4: WTI and domestic petrol prices

…but dairy prices fell in this week’s auction

Prices fell 4.2% in USD terms and 3.8% in NZD terms in the GlobalDairyTrade auction this week (Figure 5). The prices of most products fell with Whole Milk Powder down 3.9% and Skim Milk Powder down 4.9%. Dairy prices are now down 11% since the start of 2020 and 17% annually.

Figure 5: GlobalDairyTrade auction

The Reserve Bank proposes removing LVR restrictions

The Reserve Bank is proposing removing mortgage loan-to-value ratio (LVR) restrictions to enable banks to further support customers as the effects of COVID-19 unfold. The proposal is open to consultation for seven days and a decision is expected to be made soon thereafter. If the removal of LVR restrictions goes ahead, the RBNZ will not reinstate LVR restrictions for at least a year as they monitor lending activity and feedback from retail banks over the next 12 months.

Oil prices go negative

The price for the May futures contract for West Texas Intermediate (WTI) oil that expired on Tuesday traded as low as -US$40/barrel on Monday, before recovering some lost ground (Figure 6). Fundamentally, there is an excess supply of oil driven by the sudden COVID-19-related fall in demand, and there is insufficient physical storage capacity across the US for the excess supply. On the technical side, traders who had taken long positions on oil were forced to close out their positions to avoid having to take physical delivery of the oil. As a result, sellers far exceeded buyers for the May contract. The price for the June contract halved to around US$10/barrel. The weakness in the WTI market spread into broader oil markets on Tuesday, with Brent crude oil falling to its lowest level in 18 years. Saudi Arabian producers are considering whether to bring forward oil production cuts scheduled to start in May.

Figure 6: Oil prices

Growth in global infections continues to slow…

Global active cases of COVID-19 grew by 24% in the seven days ending 21 April, compared to 36% in the previous 7-day period. The US accounted for more than half of the growth in global active cases over this period.

…and some countries are preparing to come out of lockdown

Despite fears of a second wave of infections, a number of European countries have started easing their restrictions on movement and businesses (Table 1). Denmark, Germany, Switzerland, and Austria have been among the first to do so, as their infection rates have consistently declined in recent weeks. However, despite restrictions on movements being relaxed, some media reports suggest that many people are still voluntarily staying home due to the fear of becoming infected. Meanwhile, lockdowns in France and the UK are continuing, as their infection rates remain quite high. Across the Atlantic, some southern US states have started re-opening, while in Canada there are no plans yet to remove restrictions.

Table 1: COVID-19 Lockdown statuses in selected countries

Expand the table below

| Country | Lockdown status |

| Denmark | Restrictions eased gradually from 14 April |

| Austria | Restrictions eased gradually from 14 April |

| Norway | Restrictions eased gradually from 20 April |

| Germany | Lockdown to end on 3 May. Some shops allowed to open from 20 April |

| Switzerland | Approved list of businesses to open on 27 April, others to follow on 11 May |

| Italy | Plan to end lockdown to be presented this week |

| France | Lockdown extended until 11 May |

| UK | No plan to ease lockdown at this stage |

| US | Lockdown measures eased in some southern states in response to protests |

| Canada | No plan to ease lockdown at this stage |

Source: Wigram Capital Advisors, World Economic Forum, Various news reports

Policymakers attempt to cushion the blow…

Policymakers around the world have continued to try to soften the economic impact of the lockdowns by providing large amounts of fiscal and monetary stimulus. At a global level, the amount of fiscal stimulus so far is more than twice as large (at 3.7% of global GDP) than seen during the global financial crisis (Figure 7). Job retention schemes account for about a quarter of total stimulus measures, business loans and grants account for 13%, tax relief for 17%, and direct cash transfers for 11%. UBS projects that the global fiscal deficit will increase from 3.2% of GDP to 11.2% of GDP in 2020, with the largest increases expected in the US, Japan, the UK, Australia, and Italy. In the absence of fiscal stimulus, UBS estimates that global growth would have been weaker by close to 5%.

Figure 7: Change in fiscally adjusted primary fiscal balance as percentage of global GDP

…as activity remains weak

US jobless claims have topped 22 million in the four weeks since the start of its lockdown, equivalent to a decade’s worth of job creation. The New York Federal Reserve’s weekly economic index suggests that activity is down 11% compared to a year ago. The index is composed of 10 indicators, including jobless claims, retail sales, and electricity output. Meanwhile, the Chicago Federal Reserve’s National Activity Index fell to -4.2 in March, which suggests output in the US contracted soon after lockdown measures were introduced.

The Reserve Bank of Australia (RBA) Governor said in a speech that the central bank expects the economy to contract by around 10% in the first half of this year, and the unemployment rate to reach 10% by the June quarter. Minutes of the RBA’s April meeting confirmed it would keep policy extremely loose until the economy recovers. Preliminary figures from the ABS showed that retail sales were up 8.2% in March, the largest monthly rise on record, driven by panic buying – monthly turnover doubled for products such as toilet and tissue paper, flour, rice and pasta between February and March – while the effect on GDP should be neutral due to the concurrent run-down in inventories.

China’s GDP contracted sharply in Q1…

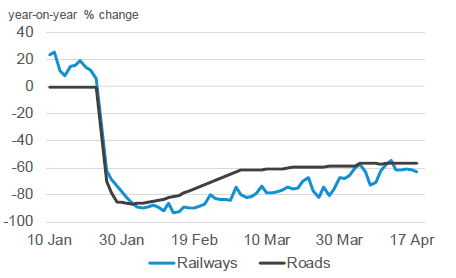

China’s GDP fell by 6.8% in Q1 compared to the same period last year – the first contraction since the country started publishing GDP figures in the early 1990s. Industrial production fell by 8.4% in Q1 on a year-on-year basis, fixed-asset investment by 16.1%, and retail sales by 19%. March activity indicators improved across the board compared to Jan-Feb, with investment returning to growth and exports performing better than expected. Daily activity trackers suggest that this recovery is likely to continue into Q2, supported by pent-up consumer demand. However, the pace of the recovery may be hampered by the global recession, supply chain disruptions, and lingering concerns about a second wave of the virus. Data from China’s transport ministry show that railway and road transport volumes remain substantially below the same period last year (Figure 8).

Figure 8: China passenger transport volume

…prompting more stimulus

Fiscal stimulus measures announced to date in China amount to a comparatively low 1.2% of GDP. Following the release of Q1’s GDP data, the authorities delivered further monetary stimulus, with the he People’s Bank of China cutting its benchmark policy rate – the one-year loan prime rate (LPR) – by 20 bps to 3.85%, and the finance ministry announced a further release of special local government bonds. Some analysts expect additional fiscal easing will be announced soon, potentially with a focus on infrastructure projects.

If you enjoyed this BFD article please consider sharing it with your friends.

{kind=link}